Flexible annuity, new CPF investment scheme recommended

SINGAPORE — After almost two years of deliberations, the panel set up to improve the Central Provident Fund (CPF) scheme has completed its work, with the unveiling of its final recommendations to help CPF members cope with inflation and provide more investment options in hopes of bolstering their retirement funds.

TODAY file photo

SINGAPORE — After almost two years of deliberations, the panel set up to improve the Central Provident Fund (CPF) scheme has completed its work, with the unveiling of its final recommendations to help CPF members cope with inflation and provide more investment options in hopes of bolstering their retirement funds.

But the intricate task of implementing these improvements — a new CPF Life option that allows for escalating payouts and an investment scheme for the less savvy — will mean it will be several years before Singaporeans can tap these options.

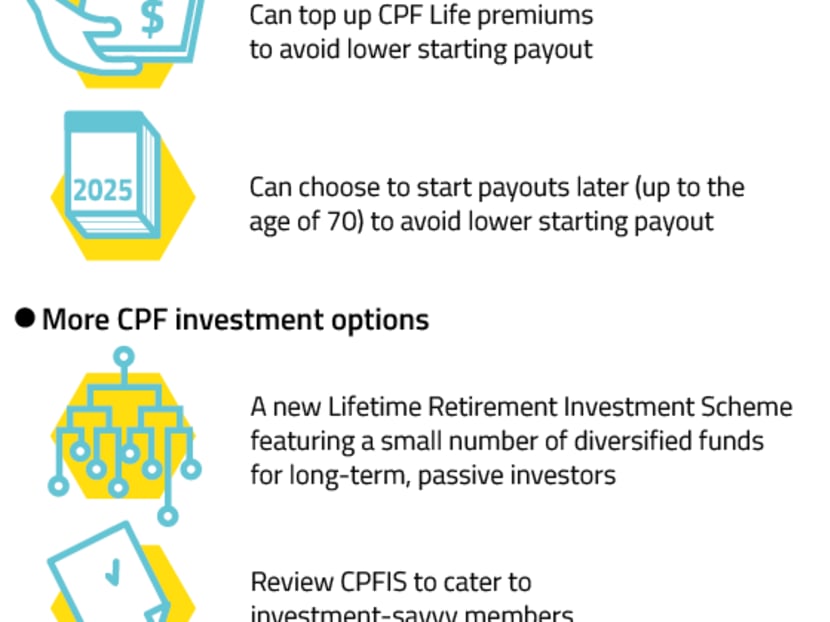

An expert investment council would have to be set up to roll out the new Lifetime Retirement Investment Scheme (LRIS), an additional investment avenue with a small array of well-diversified funds that do not require active management. The existing CPF Investment Scheme should also be reviewed to see how it can cater to shrewder members.

(click to enlarge)

Meanwhile, the new CPF Life option with payouts that will increase by 2 per cent every year would take up to two years to introduce, said the panel’s chairman Professor Tan Chorh Chuan at a media briefing on Wednesday (Aug 3), where the panel set out its considerations in crafting its second tranche of recommendations.

The 13-member panel had kept in mind that “a significant number of CPF members” wanted more flexibility to take investment risks in the hope of higher expected returns. Others wanted CPF Life monthly payouts that would rise over time to help with increases in the cost of living.

But underpinning all this was the need for simplicity — while some wanted “as much choice as possible”, it could have meant more complexity in a system “already not well understood by many”, said the panel.

As such, only two proposals were made. The new CPF Life option will see payouts start about 20 per cent lower than the payouts offered by the existing CPF Life Standard Plan at age 65. This will increase by 2 per cent a year, matching the Standard Plan payouts in 13 years and surpassing them thereafter.

Meanwhile, the new LRIS is meant as a “simpler” option, with “significantly lower fees” compared to the existing CPF Investment Scheme (CPFIS) which offers over 200 investment funds and has seen lacklustre returns mainly due to fees and sales-related costs investors had to fork out.

About half of 1,000 respondents in a telephone poll conducted last year expressed interest in this option, which filled an “important gap”, said Prof Tan, who is also president of the National University of Singapore. Consulting firm Mercer, which was roped in to analyse investment approaches, also noted that long-term investments in a diversified, low-cost fund were likely to provide better returns than the default CPF interest rates.

On the implementation timeline, Prof Tan said: “The CPF board certainly are cognisant about the need to work speedily, but bear in mind also that there are several details that will have to be looked into for both the programmes. There are different cohorts of CPF members on different types of arrangements ... LRIS will also require the appointment of an expert council and the selection of an administrator.”

The LRIS, the panel pointed out, would likely be more applicable to younger cohorts of CPF members, who have a “longer runway” to take investment risks for a higher expected return.

Accepting these recommendations, Manpower Minister Lim Swee Say penned a letter to Prof Tan, complimenting the panel for offering proposals that were “both elegant in their simplicity and far-sighted”.

“The Government will work to implement the panel’s recommendations and will proactively promote awareness and understanding of these new CPF options so that members can make informed decisions to better meet their retirement needs,” said Mr Lim.

In a media statement, National Trades Union Congress assistant secretary-general Cham Hui Fong, welcoming the changes, pointed out: “We urge the Government to ensure that proper public education and advisory services are made available to all so that members can make informed choices which best meet their needs.”

Indeed, panel member and independent actuarial consultant Colin Pakshong noted that while most people like investing their extra monies, they find themselves put off after doing their homework.

“They realise that in order to be a bit more successful in their investing, they need to do a lot of research ... (and) spend time rebalancing their portfolio to see whether it’s in line with the amount of risk they want to take on. And as they get older, they probably want to de-risk by moving into safer assets,” he said. “We can understand all of that in theory but to do it in practice is very difficult.”

The panel recommended that the Government “proactively promote awareness and understanding” of the new LRIS to eligible CPF members. “Eligible CPF members should be actively asked and reminded to choose between the CPF interest rates scheme and the LRIS,” they added.

It also noted that CPF Life continued to work well as the default annuity scheme, and there was no need to actively encourage investments in private annuities.

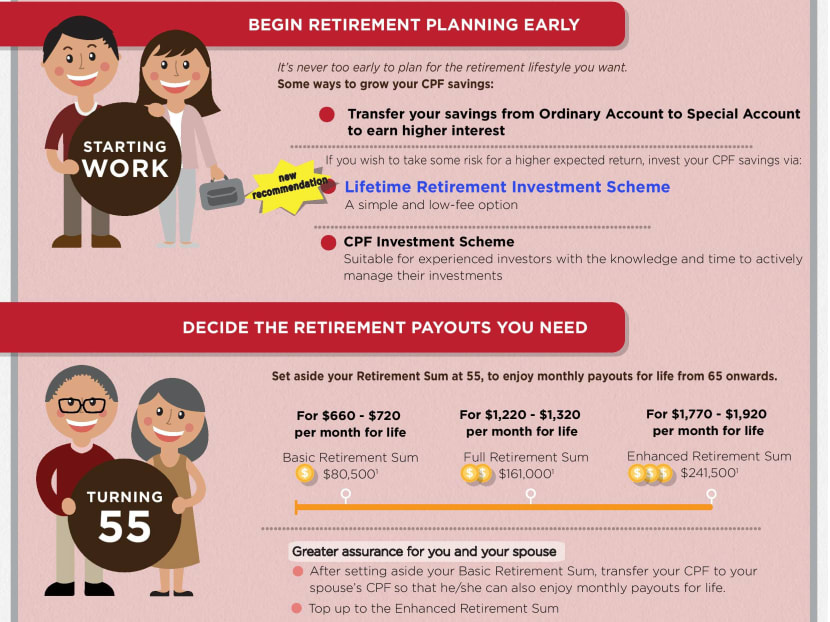

In their first set of recommendations submitted in February last year, the panel proposed three retirement sums — ranging from S$80,500 to S$241,500 — to meet differing needs, and an optional lump sum withdrawal of up to 20 per cent of their savings upon reaching age 65. Implementation started in January this year.

The second tranche of proposals were supposed to be submitted last year, but were delayed as the panel had to commission studies on overseas pension programmes and the feasibility of their own suggestions.

Asked about the targeted nature of the panel’s recommendations, Prof Tan said that it was impossible to craft a “one-size-fits-all” solution.

“The work that the panel is doing is to provide more choices that will allow you and I to do more, and have more control over our retirement planning so that it can better fit our circumstances,” he said.

Stay in the know. Anytime. Anywhere.

Subscribe to get daily news updates, insights and must reads delivered straight to your inbox.

By clicking subscribe, I agree for my personal data to be used to send me TODAY newsletters, promotional offers and for research and analysis.