What will be the impact of the latest round of property cooling measures?

The latest property cooling measures announced by the Government at close to midnight on Wednesday (Dec 15) may have come as a surprise to many. Yet the authorities have sent early warnings as early as January 2021.

The latest property cooling measures announced by the Government at close to midnight on Wednesday (Dec 15) may have come as a surprise to many.

Yet the authorities sent early warnings as far back as January 2021.

Deputy Prime Minister Heng Swee Keat and National Development Minister Desmond Lee had warned then of the possibility of more property market curbs while reiterating the Government's objective of keeping housing prices in line with economic fundamentals.

The market had already shown signs of heating up in the second half of 2020, with private home sales volume exceeding those in the same period in 2019 by about 36.4 per cent despite the pandemic.

The private residential property price index (including executive condominiums) was up by 2.2 per cent year on year (y-o-y) in the fourth quarter of 2020, even though the economy has yet to recover from the biggest crisis of a generation.

The possibility of government intervention has remained high on the property executives' radar since the beginning of the year.

A survey by the National University of Singapore’s Department of Real Estate in the first quarter of 2021 found that about 87.8 per cent of the respondents indicated possible cooling measures as a potential risk; and close to 63 per cent of them foresaw such measures to impact market sentiments adversely.

Now that the Government has taken swift and decisive action to mitigate the risk of a self-reinforcing cycle of price increases in the private and public housing resale markets, what can we make of the measures and their likely impact?

DAMPENING IMPACT OF HIKE IN ABSD RATES

The Government did not introduce new anti-speculation rules on Wednesday, but the latest round of measures further tightens the existing cooling measures, including Additional Buyers' Stamp Duty (ABSD), Total Debt Servicing Ratio (TDSR), and Loan-to-Value (LTV) rules.

Among the revisions, the increase in ABSD rates is expected to have the most significant impact on the private housing market.

The move to revise ABSD rates aims to restrain investment activities, primarily those of Singaporean citizens and permanent residents (PRs) buying second and subsequent properties as well as those of foreign investors.

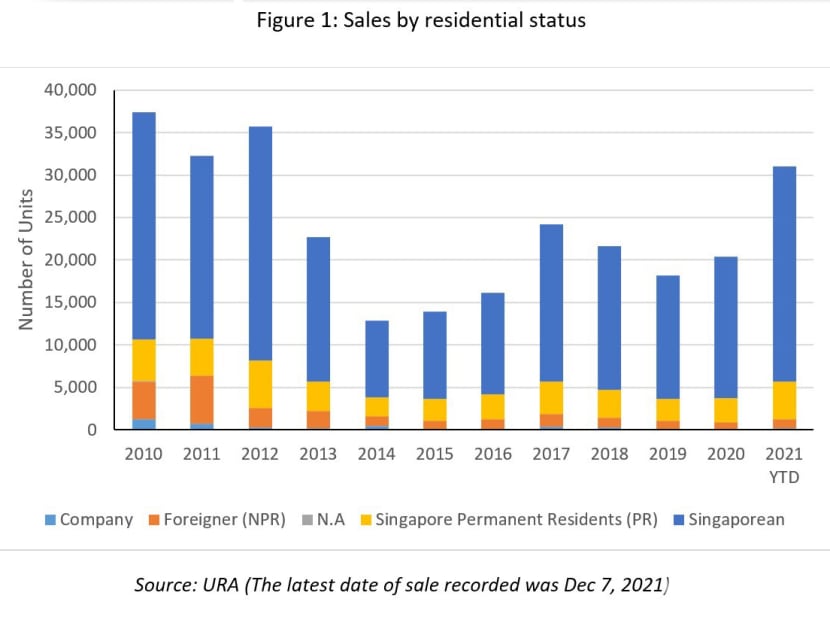

According to the Urban Redevelopment Authority’s data, demand from citizens and PRs for private homes increased significantly in 2021.

Excluding the purchases in December, the number of private home purchases by Singaporeans and PRs far exceeded the annual sales since 2014 and is close to the historical highs in 2010 (Figure 1).

The higher ABSD rates will make it more difficult for citizens and PRs to purchase second or more properties for investment purposes.

That said, there are loopholes to circumvent the ABSD payments through a decoupling arrangement, where spouses may register their purchased properties as single owners instead of joint owners.

Through decoupling, the buyers could invest in a second property either without paying ABSD (for citizens) or only paying an ABSD of 5 per cent (if one of them is a PR).

These buyers will still need to satisfy other rules such as TDSR and LTV. Foreigners' private property purchases in 2021 exceeded the pre-pandemic level in 2019 marginally.

Foreign investments in the private property market could have had been higher, if not because of the border controls and travel restrictions.

The revised ABSD rate from 25 per cent to 30 per cent for any private property purchase by foreigners will further impede foreign capital inflows into the high-end segment of the private housing market.

The revision is expected to weed out speculators who hope for short-term returns.

Under the new regime, foreign investors may have to hold and wait for their property prices to increase by more than 30 per cent to recover transaction costs and reap some investment returns.

HIT ON EN-BLOC MARKET

The higher ABSD rate of 35 per cent imposed on developers will dampen en-bloc sale activities, which have just gained some steam after several successful deals and more launching tenders for collective sales.

The revised ABSD increases development risks for licensed developers in having to fully sell their projects within five years, especially for developments on large land parcels that yield more than 500 units.

Developers also face risks of rising construction material prices, a labour shortage, and higher financing costs.

On the supply side, the authorities will ramp up the supply of new Government Land Sales sites in the coming year to ease supply imbalances and help stabilise prices.

However, the land supply effect is usually delayed due to the time involved in tender and obtaining planning approval, which generally takes between six and nine months from the launch date of a site before we could see a project launch.

FINANCIAL PRUDENCE IN ANTICIPATION OF INTEREST RATE HIKES

Borrowers overstretched financially are vulnerable to major central banks increasing interest rates in response to higher inflation and economic recovery.

The 2021 Financial Stability Review by the Monetary Authority of Singapore reports that the household debt to gross domestic product ratio remains high at 70 per cent in Q32021, and housing loan (mortgage) is the main contributor to the growth in household debt.

(The residential properties and loans account for the bulk of the household balance sheet, representing about 40 per cent of assets and 75 per cent of liabilities.)

The reduction of TDSR from 60 per cent to 55 per cent will restrict the liquidity and financing options of those buying their second and subsequent properties.

The TDSR reduction also helps protect banks against excessive financial risks, especially those with high exposure to real estate debt.

Lowering LTV from 90 per cent to 85 per cent will mean that Housing and Development Board (HDB) flat buyers taking HDB loans will need to fork out more cash in their purchases, and those who take commercial bank loans are subject to the LTV limit of 75 per cent.

Stricter LTV rules on HDB loans rein buyers in from paying excessive prices in the resale market.

Of note, HDB resale prices have increased by more than 13 per cent since the last quarter of 2020.

Overall, the slew of measures will dampen demand for homes.

Increases in the supply of new HDB flats in the coming years will address the demand by younger married couples, especially those born after the 1980s.

More GLS supply helps to ease pressure from the dwindling housing stocks in the private market and ensure that that property market is not overheated.

The measures are largely neutral to buyers with genuine owner-occupation motives, especially among first-time home buyers.

However, it is hard to design one-size-fits-all measures that meet the buyers' investment and owner-occupation needs. With higher transaction costs, investors, especially foreign ones, may have to recalibrate their strategies to ensure that their risks are well commensurate with returns on investments.

ABOUT THE AUTHORS:

Dr Lee Nai Jia is deputy director at the National University of Singapore's (NUS) Institute of Real Estate and Urban Studies. Professor Sing Tien Foo is the director at the same institute and head of the NUS Department of Real Estate. These are their own views.

Related topics

Property URA HDB investmentStay in the know. Anytime. Anywhere.

Subscribe to get daily news updates, insights and must reads delivered straight to your inbox.

By clicking subscribe, I agree for my personal data to be used to send me TODAY newsletters, promotional offers and for research and analysis.