The Big Read: Youths grappling with inflation — to save, invest or keep cash on hand?

- While rising prices cause everyone’s wallets to shrink, inflation has been said to affect youths in particular because their wages typically do not increase as fast as the cost of everyday goods

- In Singapore, the median monthly salaries of the younger age groups have gone up at a slower rate than the overall population in the past three years, with the increases between 2020 and 2021 outstripped by inflation

- From cutting down household expenses to taking on weekend side gigs, youths interviewed say they are trying to save up for their future, even as they try to maintain their lifestyles as much as possible

- On whether youths in Singapore are particularly affected by soaring inflation, economists noted that it is hard to generalise as they are not a homogenous group

- Nevertheless, for many youths, the soaring prices could mean putting off major purchases such as buying a home

- Experts offer tips on what to do when handling existing loans and to save money. They also said youths should also try set aside some money for investments

SINGAPORE — As a fresh graduate who contributes to her household expenses, 22-year-old Chin Ching Peng was faced with a dilemma: Take up her ideal job as a copywriter, or opt for a role in an unfamiliar industry that would pay higher.

“Most jobs (as a copywriter) had a salary of $2,500 or $2,800… the only one that paid more than $3,000 was for a job requiring at least two years of experience,” she said of her job-hunting experience back in February.

Ms Chin eventually took on a job in a different industry, which she declined to disclose, earlier this month, earning between S$3,000 and S$4,000 before her Central Provident Fund (CPF) contribution.

For the National University of Singapore (NUS) graduate, having a higher pay is essential since she helps out with the family budget and her mother’s medical bills. All these add up to about S$1,400 a month, but she expects it to rise further as inflation continues unabated.

“Just last year, our groceries cost about S$200 a month… but now it's almost S$300 so we must cut back. For example, prices of some vegetables at the wet market have gone up by 30 cents or 50 cents,” she said, referring to her mother’s grocery expenditure.

She also has a student loan of about S$20,000, which she will have to start repaying once the bank contacts her.

To earn some additional income for her own spending and savings, Ms Chin does freelance copywriting, earning between S$200 and S$500 whenever she gets a project. She also plans to provide Chinese tuition during weekends.

And during her scarce free time, Ms Chin stays home instead, or chooses food-and-beverage outlets with meals costing under S$20 when meeting friends.

“Sometimes, I ask my friends if we can meet next week instead because I’ve used up my entertainment budget for the week.

“Because of inflation and taking on more household responsibilities since I’ve graduated, there’s a lot of things I can’t afford,” she said.

Ms Chin is one of the many youths aged 35 and under who have had to tighten their belts or adjust their lifestyles as the daily cost of living continues to rise.

For 30-year-old sales coordinator Joyce Chiu, cutting down on unnecessary spending is crucial for she and her husband to continue saving S$200 a month from their combined roughly S$6,000 income before CPF contributions.

With three children aged nine, seven and two, Ms Chiu has cut down on simple luxuries, such as ordering a drink to accompany her meal at work, to ensure they are able to pay for their necessities without eating into their monthly savings.

“We eat out less and have a stricter budget… we also reduced our weekly fast-food treat for the kids and now do it every two weeks instead.

“Everything has gone up by 1 to 2 per cent, but when we add up the increase and multiply it by the days and months, it’s about S$50 to S$100 difference each month if we do not cut down on our spending,” said Ms Chiu.

Rising prices have been a major headache for many the past year, with headline inflation — which covers prices of all goods and services, including commodities like food and utilities — rising to 5.6 per cent in May, compared to the same month last year. This was higher than the 5.4 per cent in March and April.

Core inflation, which excludes accommodation and private transport costs, also hit its highest level in more than 13 years in May at 3.6 per cent year-on-year.

“Inflation has been said to affect youths in particular because their wages typically do not increase as fast as the cost of everyday goods. Youths also tend to consume a lot of clothing and footwear and expensive electrical items.”

While rising prices cause everyone’s wallets to shrink, inflation has been said to affect youths in particular because their wages typically do not increase as fast as the cost of everyday goods, according to a BBC report in May 2016. Youths also tend to consume a lot of clothing and footwear and expensive electrical items such as phones and tablets.

In an article published in May this year, The Conversation, an Australia-based media outlet, noted that inflation often hits lower-income households the harder as most of their income is spent on necessities such as food, housing and electricity.

And youths tend to belong to the lower-income bracket since they earn less than their older colleague counterparts, whose pay has increased over the years.

The Conversation article also noted that gig economy workers in the United Kingdom — a third of which is made up of youths aged under 34 — are also heavily affected by inflation as their monthly salaries are uncertain and they may not have employee benefits such as sick pay.

In Singapore, the pandemic had spurred a growing number of youths to enter the gig economy to make up for their loss of income, or while they were job hunting. Food delivery firm Foodpanda, for example, told TODAY in June last year that the percentage of its riders between the ages of 18 and 24 was around 10 to 15 per cent.

With youths in Singapore finding themselves in a similar predicament with their overseas counterparts, many are thus forced to be prudent with their spending when their incomes — often not as high as their middle-age working colleagues — cannot keep up with ever-rising inflation.

Median monthly salary of youths in S'pore not catching up

According to the Ministry of Manpower (MOM), youths between the ages of 20 and 24 had a median monthly salary, including employer CPF contributions, of S$2,691 last year, down from S$2,730 in 2019.

For those who were 25 and 29, they had a median monthly salary of S$4,095 last year, a mere S$14 more than the S$4,081 in 2019. Those aged 30 to 34 fared slightly better, earning a median monthly salary of S$5,222 last year, up S$25 from S$5,197 in 2019.

In comparison, the overall median monthly income in Singapore was S$4,680 last year, up S$117 from S$4,563 in 2019.

Official statistics also showed that between 2020 and last year, during the depths of the Covid-19 pandemic, youths’ pay increases were outstripped by inflation rate, further undermining their spending power.

For the age groups of 20 to 24 and 30 to 34, their median monthly incomes shrunk by 3.6 and 0.81 per cent respectively during this period, while the age group of 25 to 29 experienced a marginal increase of 0.96 per cent.

In comparison, the overall median monthly income in Singapore grew by 3.2 per cent. Last year, the Republic's headline inflation was 2.3 per cent.

On whether youths here are particularly affected by soaring inflation, economists including DBS senior economist Irvin Seah noted that it is hard to generalise as they are not a homogenous group.

Mr Seah said: “Anyone with a relatively lower earning power and slower increase in income compared to the vast majority of the population will be more vulnerable to the impacts of inflation… so these are typically the low income, the elderly and also, the youth."

He added: “But for youths who have just started working, some have less financial commitments, and the labour market has been very tight so there are more job opportunities. They may also be able to get better compensation packages, but this depends on their industry and jobs.”

Maybank economist Lee Ju Ye also noted that youth employment has improved in recent years: Resident youth unemployment rate fell to 5 per cent in the first quarter of this year, which is even lower than the pre-pandemic level of 5.8 per cent in the first quarter of 2019.

Still, she pointed out that with inflation rising at the fastest pace in a decade, "this would likely be the first time youths below 35 years old experience living costs rising this high since the start of their working lives”.

“This would likely be the first time youths below 35 years old experience living costs rising this high since the start of their working lives.Maybank economist Lee Ju Ye”

In particular, young property hunters or owners may feel the impact of inflation more keenly, said Mr Bernard Aw, economist for Asia Pacific at credit insurer Coface.

“An important consequence of high inflation is tighter monetary policy that contributes to higher interest rates, which we are already experiencing in Singapore," he said.

“If the trend of rising interest rates continues in order to contain inflationary pressure, this will impact youths who are searching for their first homes or those that have just purchased their homes with a bank loan.”

COPING WITH INFLATION: EAT OUT LESS, STAY HOME MORE

Some fresh graduates who are just starting to embark on their next journey in life are trying to tame the inflation beast in their own ways.

While the likes of Ms Chin have cut down on most of their expenses or taken on side hustles to bolster their nest eggs, others have chosen to dig into their savings.

Mr Wei Chen Kun, 24, who graduated from NUS last month, has yet to start searching for a full-time job but earns about S$1,000 from giving tuition.

Of that amount, about S$200 goes towards paying the rent for a master bedroom, which he shares with his mother, in a condominium.

However, his landlord has doubled their rent from this month, citing an “uncertain economy”. Now, he and his mother — who are both Chinese nationals — are considering renting another home to reduce their monthly expenditure.

“Even eating out costs more, especially adding an egg to a meal. It used to be 50 cents, but now it can be up to S$1 when dining out,” said Mr Wei, who typically saves about S$700 each month. His mother, who also works, would pay for the rest of their household expenses.

He also had to use his savings to pay for his graduation trip earlier this month, which cost him “somewhere in the four-digit range”.

“Graduation trips are a once-in-a-lifetime experience, so I don’t want to sacrifice this despite rising costs,” he said.

Apart from the 20-somethings who are starting out with less, even some of those in their 30s are feeling the inflationary heat.

Ms Jaya Devi, 34, who has been working as a financial consultant for three years, earns about S$2,500 a month as her income is fully dependent on commissions.

When her father died in 2019, she became the household’s breadwinner and took over the responsibility for the family’s mortgage. Her brother is married and does not contribute to the household expenses.

While she is able to use her CPF to pay for its monthly installments, she has stopped making CPF contributions as her household expenses have risen in recent months.

“I used to contribute S$200 into my CPF since I’m considered self-employed but I stopped in June because my mother needs more money to buy our groceries,” said Ms Jaya.

Despite cutting back on outings with her friends and using public transport more, Ms Jaya has been withdrawing between S$100 and S$200 each month from her savings since April to finance her increased household expenditure. But she plans to stop doing so by the end of the year as she wants to ensure she has some money left for emergencies.

While she has tried to increase her work hours, finding customers has been tough. “Everyone is facing the crunch of inflation, so their buying power has decreased,” she said

“I actually set a goal to pay off the S$80,000 mortgage on our house by next year… so I don’t burden my mother but now, I don’t think it’ll be possible to hit that timeline so soon."

At the other end of the earnings spectrum, 34-year-old financial adviser Kng Zhi Han makes between S$10,000 and S$12,000 a month, and puts aside at least 50 per cent of his income into savings.

But this comes with a price of its own — eating out less, and switching to using house brand items. Mr Kng, who is living with his parents, also has to pay for his monthly car loan and contributes S$500 to his household expenses.

“I need to drive a lot to meet my clients for work, but fuel prices have gone up,” he said.

While he would typically spend S$60 for a week’s petrol in January, the amount is now around S$80.

Mr Kng had considered moving out of his parents’ house to gain more independence and privacy. But with rents going up in the past few months, he is in two minds about whether the move would be worth the significant increase in monthly commitment on rent.

“Two years ago, (rentals for) condominium units cost around S$3,000 a month in a central city location. Now, it’s probably between S$5,000 and S$6,000,” he said.

While the likes of Mr Kng grapple with issues like high rents, those with young children have other concerns to deal with.

While 29-year-old IT project manager Alex Goi makes between S$7,000 and S$8,000 a month, his two-year-old son’s expenses have risen significantly in the past few months. His wife earns between S$2,000 and S$3,000.

“Diaper prices have gone up because the brands now sell fewer pieces in a pack,” said Mr Goi, noting that his son’s diapers now cost S$1 each, double what it was a year ago.

He added: “Wyatt’s (his son) milk powder used to be S$80 a tin about five months ago, but now it's S$100 a tin. We can’t switch to cheaper brands because children are picky, and we also don’t want to risk his health by making sudden changes.”

The rising cost of living— which had Mr Goi spending S$1,000 more in May compared to April — has spurred him to change his lifestyle recently.

The family now goes out once every two weeks, instead of weekly, on a budget of S$100, half of what they would have previously spent. They also cook more at home to avoid eating out.

“Our medical premiums have also gone up, so I’m looking to reduce our coverage to cut down the cost of medical insurance,” said Mr Goi.

“We’re also hoping to save up more to pay for our Build-to-Order (BTO) flat. But its completion date has been delayed to 2025, and we’re unsure if we’ll have to start renting in the open market since our incomes are now past the rental ceiling."

The couple pays S$600 a month renting a flat from the Housing Development Board under the Parenthood Provisional Housing Scheme, and had signed their lease before the income ceiling of S$7,000 was introduced at the start of 2022. Their lease will end late next year.

“It’s definitely a concern that we’ve had to lower our standard of living and make so many cuts.IT project manager Alex Goi, 29”

“It’s definitely a concern that we’ve had to lower our standard of living and make so many cuts,” Mr Goi said.

Similarly, Ms Chiu, the 30-year-old sales coordinator, has had to make sacrifices as her children’s expenses have increased.

She currently gives her two primary-school-going children S$4 a day, of which they are expected to save S$1 as she hopes to instill the thrifty habit in them.

“Now, I don’t know if they can save S$1 because they need to eat and will want a snack or fruit,” she said, referring to news last week that school canteen food prices were set to rise, after the Ministry of Education revised pricing guidelines in response to higher costs.

With SP Group raising electricity tariff for households by an average of 8 per cent for the July to September period, compared with the previous quarter, it also means a S$20 to S$30 increase in monthly spending for Ms Chiu's household.

Ms Chiu has put on hold her plans to take a family vacation to Malaysia as they tighten their belts further.

“Things will be alright because we can all do this together as a family, but it's not going to be as easy as before unless our pay increases,” she said.

WITH PRICES OF EVERYTHING GOING UP, BEING PRUDENT IS KEY

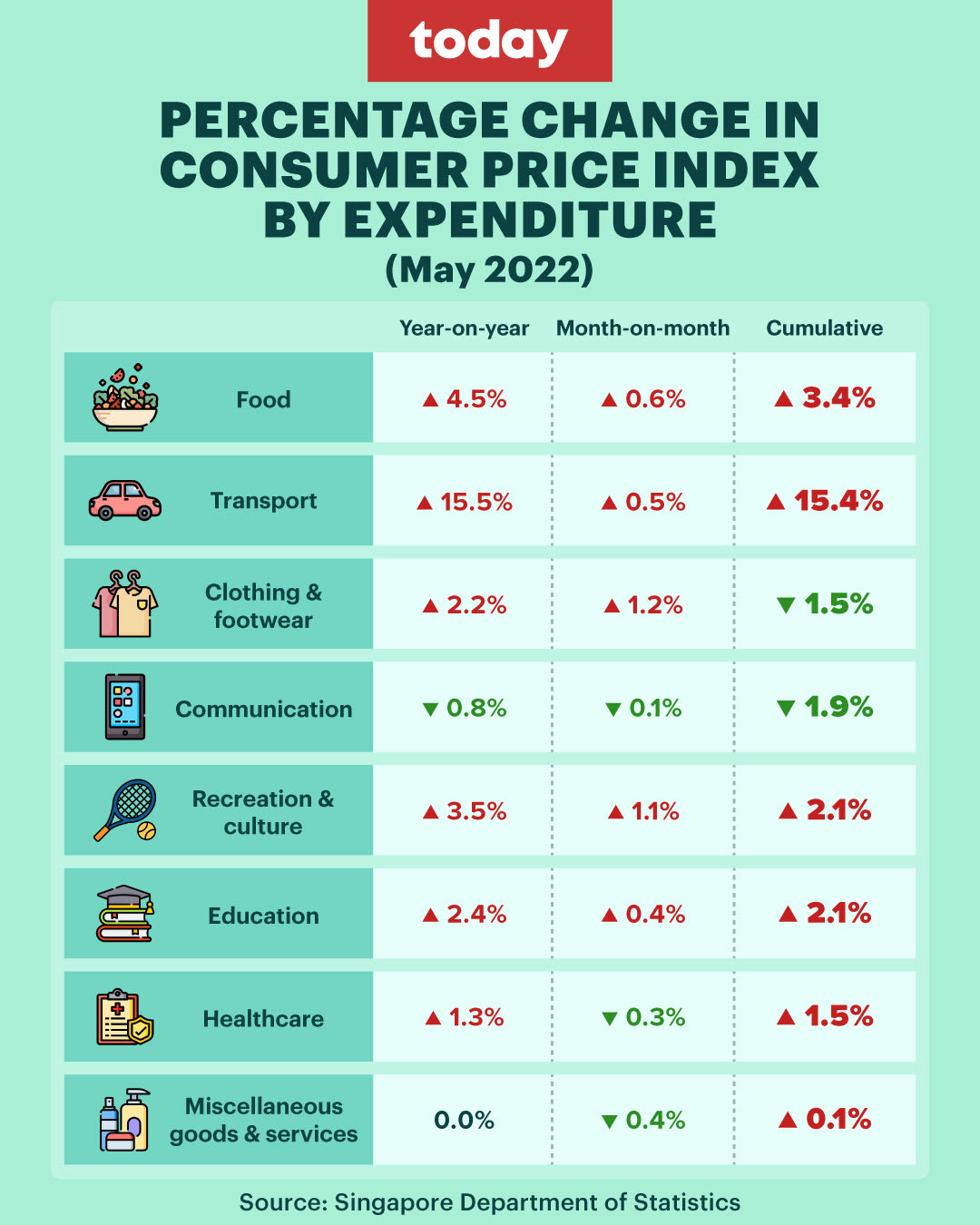

According to the Singapore Department of Statistics, the Consumer Price Index for all sectors except communications increased in May year-on-year. The index measures the average price change for household goods and services commonly purchased over time.

The highest increase was in transportation (15.5 per cent) amid rising fuel prices and Certificate of Entitlement premiums. Food prices have also jumped by 4.5 per cent year-on-year, amid disruptions to export partly due to the war in Ukraine.

Meanwhile, median mortgage rates in Singapore in May have nearly doubled compared with December last year. This comes as central banks worldwide increase interest rates to combat inflation, with the United States Federal Reserve announcing its biggest hike in its benchmark interest rates in two decades on May 4.

Two young homeowners told TODAY they had received letters from banks that their interest rates would be increasing, though they were not worried as they had budgeted enough for such situations.

Rents have also increased, with four tenants telling TODAY their monthly payment has increased by S$100 to S$300 this year.

Mr Pow Ying Khuan, head of research at 99.co, said that increased demand for rental units can be attributed to supply shortages due to construction delays and fewer homeowners willing to rent out their homes with Covid-19 still lurking everywhere.

Citing the 99-SRX rental indices, he said that overall condo rents had increased by 18.1 per cent in May year-on-year.

Overall, HDB rents have also increased for 23 months straight, climbing 16.2 per cent between May this year and the same month last year. “With a robust labour market, strengthened Singapore dollar and reopened borders, expats have also been more inclined to move to Singapore for work as they compete with the locals for rental units,” Mr Pow said.

Ms Christine Sun, senior vice president of research and analytics at OrangeTee and Tie, noted that demand for rental also rose as more households looking to upgrade their homes switched to renting after selling their flats, in order to avoid paying the additional buyers’ stamp duty when purchasing a new property.

Providing advice for tenants, Ms Sun said that they can negotiate lower rentals by signing longer leases. As for property hunters, they can consider delaying their purchases as there will be “as many as 20,000 private homes will be completed in 2023, up from the 10,401 units this year”.

Mr Ong Teck Hui, senior director of research and consultancy at JLL Singapore, said: “A major risk to homeowners is the loss of one’s job and income that would lead to a mortgage default. Therefore, it would be prudent to ensure a level of savings that can help towards mortgage repayments, at least for a certain period before one regains employment.”

Aside from homeownership, finance experts previously interviewed by TODAY in April gave some general tips that can help Singaporeans through the rising costs of living. Families, for example, can better keep track of household expenditure by reviewing their finances regularly.

WHAT TO WATCH OUT FOR WHEN TAKING LOANS

When it comes to refinancing loans to help families ease inflation-induced financial stresses, Mr Nelson Neo, head of home financing solutions at DBS Consumer Banking Group, said that while this is an option, homeowners should know the costs involved, such as the legal fees and valuation costs.

“Regardless of interest rate trends or choice of home loan packages, we strongly advise borrowers to set aside sufficient funds as a buffer in case of further interest rate hikes or any unforeseen circumstances,” said Mr Neo, adding this would ideally be a buffer for about two years.

While getting a loan may help youths tide through tough times of financial need, experts also warned the need to exercise prudence.

Noting that taking up a loan is a “significant financial commitment” over a period of time, Mr Anthony Seow, head of payments and platforms at DBS Consumer Banking Group, said youths should ensure they have the ability to repay their loan, and if possible, increase their loan repayments to lower their interest payable.

He said they should also look out for fees and charges, flexibility of loan repayments and the loan’s lock-in period, noting that some loans have penalties for paying it up earlier than agreed.

“Any late payment or repayment difficulties may be reflected in your credit score and records, and adverse records may impact your future financing needs,” said Mr Seow.

IS IT A GOOD TIME TO INVEST?

With a one-month-old newborn, a housing loan to pay and three businesses under his belt, 32-year-old property agent and business owner Jonathan Ong has stopped making risky investments in the stock market and crypto scene.

“I was lucky enough to cash out before the crypto crash and stock prices dropping, but right now there’s too much risk in not having enough cash on hand,” he said.

He runs restaurant Daddy On Madras, a virtual tour company Metaspace, and is working on a real estate application called Homee SG — all of which have seen profit margins shrink as people spend less and cost of goods rise.

As for 25-year-old lead executive Jessica, who declined to reveal her surname, saving up for her further studies has become tougher due to inflation.

She added: “I had been considering taking up more long-term investment plans, but with inflation, I don’t want to do it because they can’t be easily accessed or used should I need it for an emergency.

“The interest rates for long-term investment plans also seems bad when compared to the current rate of inflation.”

“If inflation is high, choosing not to invest means that any savings you have will be losing its purchasing power over time.Mr Timothy Ho, co-founder and managing editor of investing website Dollars and Sense”

However, experts said that it is important for youths to start investing for their future, should they have enough savings on hand.

Mr Timothy Ho, co-founder and managing editor of investing website Dollars and Sense, said: “If inflation is high, choosing not to invest means that any savings you have will be losing its purchasing power over time.

“As a young person, our biggest advantage is age. We can easily invest today in good companies and hold for 20 or even 30 years, without worrying about having to sell them as long as we have our emergency savings and manage our finances well."

Far from looking for the shiny new toy, Mr Ho stressed that "investing should be dull, not exciting".

"Any investments you make today ought to be investments you are willing to hold on to even if the prices decline in the short to midterm," he said.

Mr Ho suggested that young working adults should set aside between six to nine months of their monthly average expenses before they invest, so that they have funds for rainy days.

For youths looking to make short-term investments, some less risky assets include the Singapore Savings Bonds, Money Market Funds and short-term endowment plans, he said.

He added that youths who are just starting to invest should treat it like "learning any other life skills... start out slow and build confidence over time".

CIMB Private Banking economist Song Seng Wun said that youths should avoid biting off more than they can chew.

He added: “There’s no such thing as a free lunch, the larger the investment risk, the larger the payout or loss. One big lesson is the spectacular rise and fall of the crypto space, which we are still seeing its consequences unfold.”

“While it is not wrong to take risks, it should be a calculated risk rather taking it on blindly because of the promise of returns," he said.

Long-term investment plans may seem boring, but “boring returns compounded can make a difference years down the road”, he reiterated.

Related topics

inflation Youth economy household the big readStay in the know. Anytime. Anywhere.

Subscribe to our newsletter for the top features, insights and must reads delivered straight to your inbox.

By clicking subscribe, I agree for my personal data to be used to send me TODAY newsletters, promotional offers and for research and analysis.