Caution needed for vulnerable groups in taking on more debt, though most households resilient to income, interest rate shocks: MAS

SINGAPORE — Even though most households appear financially resilient, the Monetary Authority of Singapore (MAS) warned that some households are found to be more vulnerable to adverse income and interest rate shocks, and they need to be cautious about taking on more debt in view of higher interest rates and increased economic uncertainties.

- Most Singapore households appear resilient to income and interest rate shocks, the Monetary Authority of Singapore said in its annual financial stability review

- However, vulnerable households such as those with a lower income need to be cautious about taking on more debt in the current economic environment

- Personal savings, which refers to the amount of money available after consumption and before the purchase of assets, have also declined

SINGAPORE — Even though most households appear financially resilient, the Monetary Authority of Singapore (MAS) warned that some households are found to be more vulnerable to adverse income and interest rate shocks, and they need to be cautious about taking on more debt in view of higher interest rates and increased economic uncertainties.

MAS said in its annual financial stability review that these vulnerable households are those that have larger outstanding mortgage loans, are more leveraged (in debt), or have lower incomes.

"Such households tend to be in the lower-income deciles and have limited financial buffers," it said in the report released on Friday (Nov 25).

"Households should therefore exercise prudence in their finances, including mortgage loan obligations, to cushion against tightening financial conditions ahead," the central bank cautioned.

MAS noted in its report that household financial vulnerabilities have worsened in the third quarter this year, primarily due to more short-term debt, represented by credit card borrowings.

Household leverage risk has also risen slightly, but has remained in the same band as the same period last year.

Overall, though, MAS' stress tests suggest that most households should remain financially resilient even under scenarios of significant income loss or sharp interest rate hikes.

"Looking ahead, Singapore’s household sector is assessed to have sufficient positive equity and liquidity to mitigate downside risks in the event of falling asset values and rising debt servicing costs," MAS said.

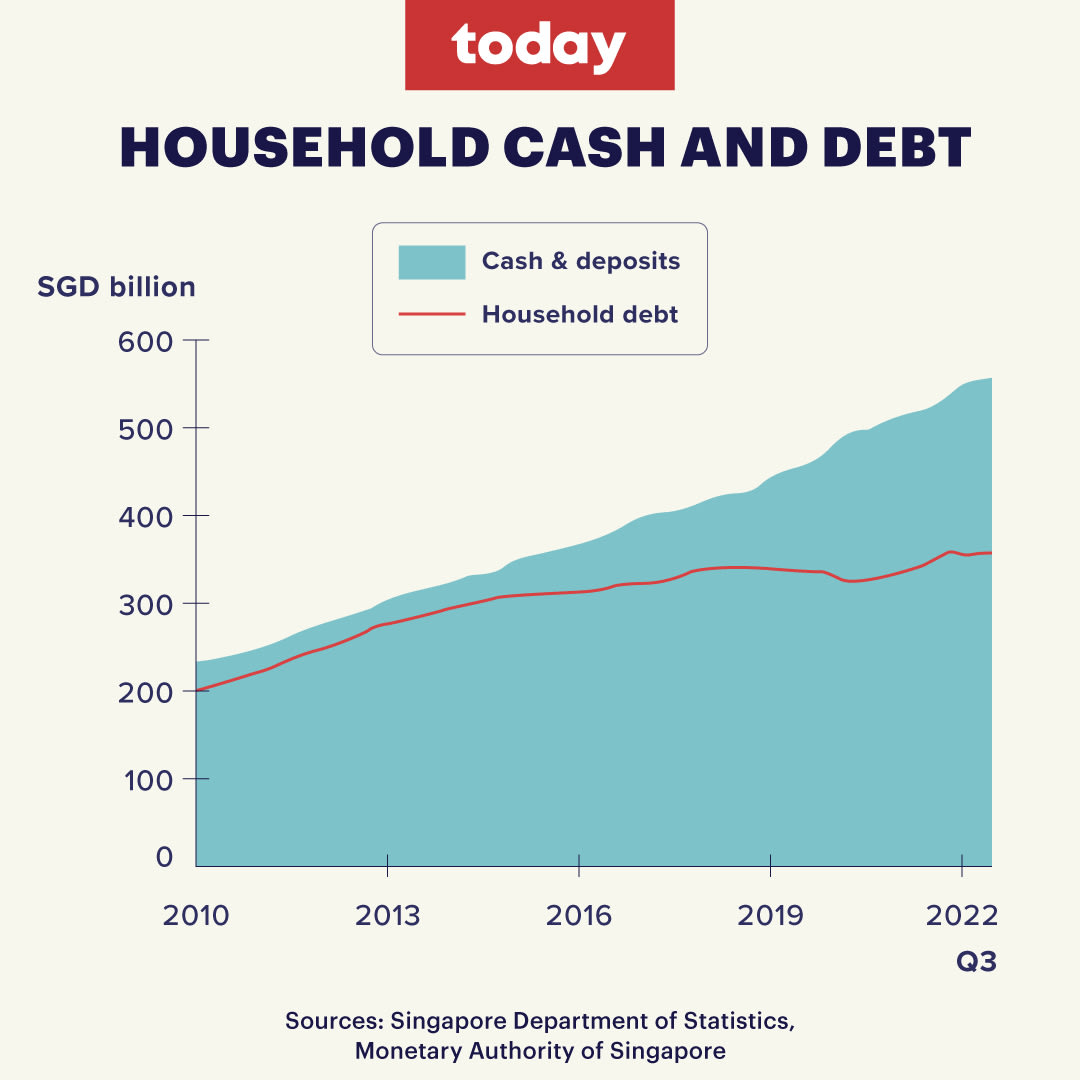

The household sectors net wealth had "remained strong" over the past year, rising by 7.5 per cent year-on-year to S$2.5 trillion in the third quarter this year.

This increase is supported by continued growth in residential property assets, with residential property assets contributing 5.3 percentage points to the overall 6.9 per cent growth of total household assets in the third quarter.

However, personal savings, which refers to the amount of money available after consumption and before the purchase of assets, have declined. The personal savings rate fell to 35 per cent in the third quarter, after peaking at 40 per cent in the first quarter of 2021.

"This reflected the strong growth in private consumption expenditure with the easing of Covid-related restrictions," MAS said.

Friday's report followed a parliamentary reply in August this year by Senior Minister Tharman Shanmugaratnam, who said that Singapore households' ability to meet their immediate debt repayment obligations is healthy, with deposits growing faster than total household debt. Mr Tharman is also chairman of MAS.

He also noted at the time that there was a small segment of households who were more highly leveraged and could face difficulties in servicing their debt.

The financial vulnerability of households is determined by two factors: Leverage risk (largely due to debt from housing loans) and maturity risk (largely due to debt from credit card balances).

HIGHER MORTGAGES AFFECT HOUSEHOLD FINANCIAL STABILITY

MAS said that housing loans remained the key driver of the rise in household debt, contributing 2.7 percentage points to the overall 3.1 per cent year-on-year growth in debt for the third quarter this year.

"Outstanding housing loans have seen sustained growth since 2021, although it has remained broadly stable in recent months, following the tightening of the headline Total Debt Servicing Ratio threshold at end-2021."

Following the decline in the first quarter of 2021 as a result of the tightening measures, new housing loans had since gradually picked up in subsequent quarters, "mirroring transaction activity in the private residential property market", it added.

Despite the sharp increase in mortgage rates since early 2022, private residential property prices have continued to rise, with property prices growing by an average of 2.7 per cent in the first three quarters of 2022 on a quarter-on-quarter basis, slightly higher than the average gain of 2.6 per cent in 2021.

At the same time, the increase in property prices was supported by transaction volumes that have remained higher than pre-Covid levels.

The easing in property market-related safe management measures (for Covid-19) since the second quarter this year facilitated viewings of homes and developer sale galleries, contributing to the increase in sales," MAS said.

The 2022 average quarterly transaction volume as of the third quarter this year was about 28 per cent lower than in 2021, but remained 10 per cent higher than pre-Covid levels between 2017 and 2019, and were driven largely by resident demand.

Although the private residential property market "has remained resilient" over the past year, there are still elevated interest rates, and increased downside risks to global growth could weigh on market sentiments in the coming quarters, MAS added.

At the same time, the ramp-up in the supply of private housing via the government land sales this year will help ease demand pressures when the development projects are ready for sale in 2023.

"The Government will be vigilant to market developments with the continuing objective of promoting sustainable conditions in the property market."

CREDIT CARD DEBT UP 16 PER CENT

Maturity risk has increased with the rise in short-term debt, MAS said.

Households’ short-term debt, as represented by outstanding credit card balances, has increased 16 per cent year-on-year in the third quarter, the strongest increase since 2011.

Outstanding credit card balances as a percentage of personal disposable income also rose slightly to 4.1 per cent in the third quarter.

"Accordingly, household maturity risk has risen with the increase in unsecured credit, reflecting the boost in discretionary spending as the easing of Covid-related restrictions released pent-up demand," MAS said.

However, the credit quality of short-term debt has remained healthy, MAS noted. Credit quality is a measurement of an individual's ability to repay their debt.

On the other hand, in another positive sign, the credit card charge-off rate, which refers to the bad debts written off divided by the average rollover balance, declined to 3.5 per cent in the third quarter.

The rollover balance increased by 11.2 per cent year-on-year in the third quarter, while the amount of bad debt written off has fallen continually since 2021.

Bad debt refers to loans or outstanding balances owed that are no longer deemed recoverable and must be written off.

"That said, the charge-off rate is likely to normalise to pre-crisis levels as the relief measures have been withdrawn," MAS said.

HOUSEHOLD DEBT SERVICING

MAS said in its report that households face higher borrowing costs as domestic interest rates rise in tandem with global interest rates.

Domestic Singdollar interbank interest rates, in particular, have risen sharply this year.

For instance, the three-month compounded Singapore Overnight Rate Average (Sora), which is a key benchmark for mortgage rates, increased from near-zero levels at the start of the year to about 2.6 per cent in mid-November this year.

"Correspondingly, mortgage rates for both floating-rate and fixed-rate packages have risen by about the same extent to around 3.5 per cent and 4.5 per cent respectively over the same period," MAS said.

"Market-based forward prices suggest that Sora-based mortgage rates could rise further in the coming months, before stabilising at levels that will still be significantly higher than the low rates seen in the last decade."

Therefore, MAS said that households will face higher loan repayments, with the magnitude of increase escalating with the size of mortgages.

However, MAS said in the report that its stress tests show that households’ debt servicing ratios "remain manageable under a conservative scenario of a reduction in income on top of interest rate shocks".

"Specifically, even under the scenario of a simultaneous and immediate 400 basis points increase in interest rates, and a 10 per cent reduction in income, most households are expected to be able to continue servicing their debt."

MAS also noted that for vulnerable households, such as new borrowers with larger outstanding mortgage loans, tend to be more leveraged and face greater risk of cashflow strains.

It noted that such households face even higher risks if they are of lower income with limited financial buffers. This is because such households "typically also have higher expenditure-to-income ratios".

"The tightened credit measures of the lower Total Debt Servicing Ratio threshold and higher credit assessment interest rates would ensure that new borrowers continue to be financially prudent," MAS added.

RISKS TO CORPORATES

MAS also said in its report that corporate vulnerability to economic shocks has "increased slightly".

The maturity risk of debt has also edged up for firms, but they have enough liquidity reserves to cover short-term liabilities, MAS added.

Leverage risk has also eased because corporate sector debt as a share of the gross domestic product has fallen.

At the same time, foreign currency mismatch risk has remained stable as Singapore firms continue to avoid over-reliance on borrowing foreign currency.

This risk relates to the impact of changing exchange rates to a company's financial position.

In the meantime, the vulnerability of the financial sector has increased over the past year, largely driven by "rising leverage vulnerabilities as banks’ balance sheets expanded alongside the recovery in economic activity".

Related topics

household debt MAS economyStay in the know. Anytime. Anywhere.

Subscribe to our newsletter for the top features, insights and must reads delivered straight to your inbox.

By clicking subscribe, I agree for my personal data to be used to send me TODAY newsletters, promotional offers and for research and analysis.