Explainer: Why Sora is likely to replace Sibor as Singapore’s benchmark interest rate

SINGAPORE — The Singapore Interbank Offered Rates (Sibor) — the benchmark interest rate in Singapore — could be discontinued in the next three to four years and replaced by the Singapore Overnight Rate Average (Sora).

A report stated that shifting to the Singapore Overnight Rate Average will result in more transparent loan market pricing for borrowers, and more efficient risk management for lenders.

- Singapore’s benchmark interest rate, known as Sibor, to be discontinued by 2024

- Industry group proposes Sibor to be replaced by Sora in consultation report

- The shift to a uniform benchmark interest rate would facilitate a more transparent pricing of loan packages for consumers, the report said

SINGAPORE — The Singapore Interbank Offered Rates (Sibor) — the benchmark interest rate in Singapore — could be discontinued in the next three to four years and replaced by the Singapore Overnight Rate Average (Sora).

This was the recommendation by three financial industry groups that released a consultation paper on Wednesday (July 29).

Their suggestion comes after a year of transitional testing in a quest to reform Sibor to a new benchmark rate — termed the new polled benchmark in the report — and the results showed that a seamless transition would not be possible.

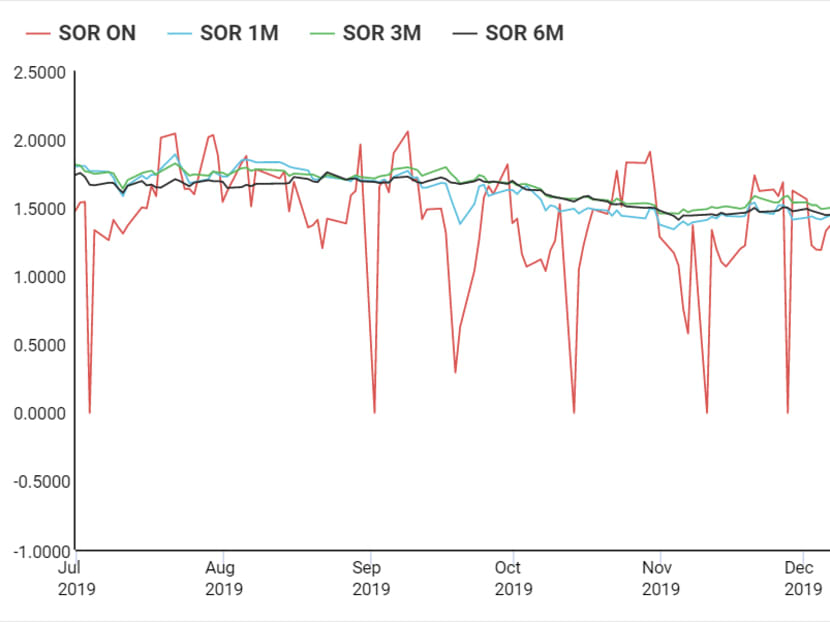

Given that another widely used rate known as the Singapore dollar Swap Offer Rate (Sor) was to be replaced by the Sora when it is discontinued by the end of 2021, the report recommended adopting a single rate for the Singapore dollar financial markets with Sora as the new benchmark rate, instead of having multiple rates.

The consultation paper, which was put together by the Association of Banks in Singapore (ABS), the Singapore Foreign Exchange Market Committee and the Steering Committee for Sor Transition to Sora, is seeking feedback from the industry until Sept 30.

They are aiming to finalise the changes and to confirm the discontinuation date for the one-month and three-month Sibor — which are widely used interest rates in many loans — by the end of this year.

TODAY explains why the consultation paper proposed the change from Sibor to Sora as Singapore’s benchmark interest rate, and how consumers will be affected.

WHY THE NEED FOR CHANGE?

Plans to reform Sibor to a new benchmark rate started in December 2017, when it was found that the practice of banks borrowing from each other declined in importance as a source of funding, due to regulatory changes imposed on banks after the 2008-2009 global financial crisis.

Instead of basing it on how banks are lending each other, the team that started Sibor’s reform in 2017 came up with a methodology that included corporate deposit transactions as part of the design of Sibor’s successor. It still relied on the banks’ use of expert judgement, though of a lesser degree.

However, after a year of testing, they found that this supposed new benchmark rate was more volatile than Sibor and did not track as closely to Sibor’s movements as anticipated.

Hence, the new polled benchmark would not be able to replace Sibor seamlessly and there would be extensive amendments to existing Sibor contracts, a process that would be “significantly more complicated and resource intensive”, the report said.

Given that the industry was already transitioning from Sor to Sora as the benchmark rate in the derivatives market and it was achieving “good progress”, the report said, it recommended moving Singapore-dollar financial markets to a single rate regime focused on Sora.

As the US dollar London Interbank Offered Rate (Libor) will cease at the end of 2021, it means that Sor will have to be discontinued as well given how it is computed with US Libor. Sora was identified to replace Sor in August 2019.

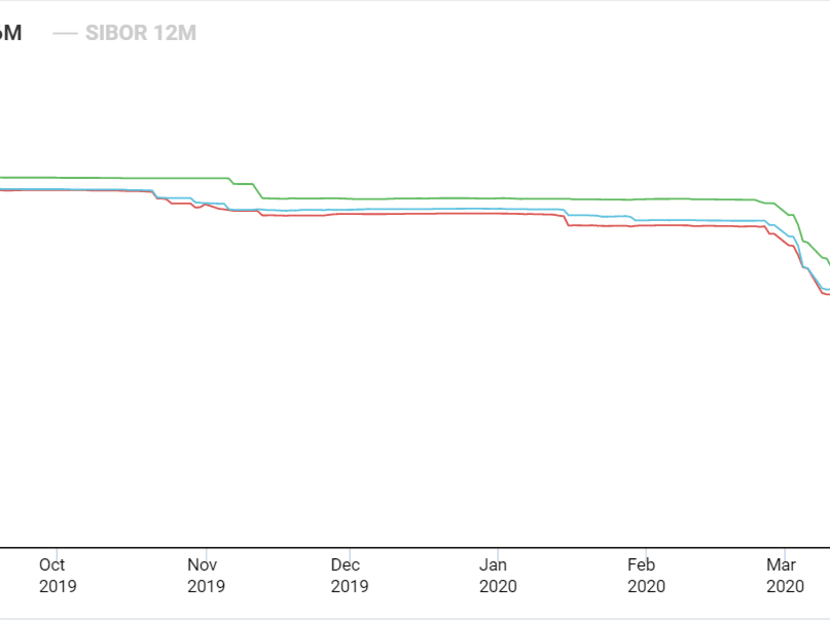

Sora is the rate of unsecured overnight interbank Singapore-dollar transactions in Singapore and its rates have been published on the website of the Monetary Authority of Singapore (MAS) since 2005.

WHY CHOOSE SORA?

The report stated that shifting to Sora will result in more transparent loan market pricing for borrowers, and more efficient risk management for lenders.

It made its recommendation based on the following five reasons:

Consumers can compare different loan packages more easily with a uniform interest rate benchmark landscape and Sora is of comparable volatility to Sibor

Banks face lower risks than when they have to use different reference rates for different financial products

It would result in a wider use of Sora and help push the development of Sora markets, as well as prevent a more bifurcated financial market

Sora is more sustainable as it is computed purely from banks’ transactions without any expert judgement required

International financial markets are increasing the usage of interest rates similar to Sora

HOW ARE CONSUMERS AFFECTED?

Given Sibor’s impending discontinuation by 2024, the industry groups behind the report recommended that consumers looking to take on a new loan consider using other reference rates, such as fixed rate packages determined by the banks, or other floating rate packages.

This is to avoid having to transition out of Sibor contracts in the future when it is soon to be discontinued.

“If customers continue to have a strong preference to enter into new Sibor contracts during this interim period, it is critical that appropriate contractual fallbacks are incorporated, to minimise the risk of contract frustration at Sibor’s eventual discontinuation,” the report said.

For existing customers on one-month, three-month and six-month Sibor contracts, there would be no immediate impact.

The report recommended that banks transition out of Sibor contracts in phases.

As contracts pegged to the six-month Sibor is not widely used, the transition can take place before the end of 2021.

The report suggested that the six-month Sibor be discontinued when the six-month Sor is terminated, or shortly after. The six-month Sor is pegged to the six-month Sibor.

The 12-month Sibor, a rate that is not widely used, will be discontinued by the end of this year as announced earlier by ABS.

As for one-month and three-month Sibor contracts, the report recommended that banks start the transition after the Sor-to-Sora shift in the derivatives market is completed in 2021.

Responding to a query on whether the switch would mean that consumers would have to pay higher interests, Mrs Ong Ai-Boon, director of ABS, said that benchmark interest rate is an independent reference rate that reflects market conditions.

But the full price of a loan is dependent on the all-in rate, which includes factors such as the banks' cost of funding and the customer’s credit profile.

“The full cost of the loan package doesn’t necessarily change when a customer chooses a different benchmark rate,” she said.

Related topics

Sora ABS Sibor banks interest rate loanStay in the know. Anytime. Anywhere.

Subscribe to our newsletter for the top features, insights and must reads delivered straight to your inbox.

By clicking subscribe, I agree for my personal data to be used to send me TODAY newsletters, promotional offers and for research and analysis.