Rising mortgage rates unlikely to dampen property demand until they climb above 3%: Analysts

SINGAPORE — The recent bank hikes on mortgage rates are unlikely to dampen demand for both public and private properties unless the rates edge past 3 per cent, several property analysts said. For now, this meant that property prices will continue to soar.

- Property analysts told TODAY that the current mortgage rates are still manageable

- They do not expect home buyers to feel the bite until it edges past 3 per cent

- Even then, one analyst says it is matter of tempering expectations and it will not deter a “genuine homebuyer”

SINGAPORE — The recent bank hikes on mortgage rates are unlikely to dampen demand for both public and private properties unless the rates edge past 3 per cent, several property analysts said. For now, this meant that property prices will continue to soar.

They were commenting on the second quarter residential property transactions data released on Friday (July 22) by the Housing and Development Board (HDB) and Urban Redevelopment Authority (URA).

In April to June this year, there were 6,819 resale transactions for public flats, a 1.7 per cent decrease from the 6,934 transactions recorded in the previous quarter.

Meanwhile, resale prices for public homes rose 2.8 per cent from the previous quarter, which is slightly higher than the 2.6 per cent in flash estimates provided by HDB earlier this month.

The resale price index, which provides information on the general price movements in the resale public housing market, was 163.9 in the second quarter — an increase from 159.5 in the previous quarter.

As for private homes, prices rose at a quicker pace of 3.5 per cent in the second quarter of this year, five times the 0.7 per cent increase in the previous quarter.

The private residential property price index increased to 180.9 in the second quarter, up from 174.8 in the preceding three months, according to URA’s data.

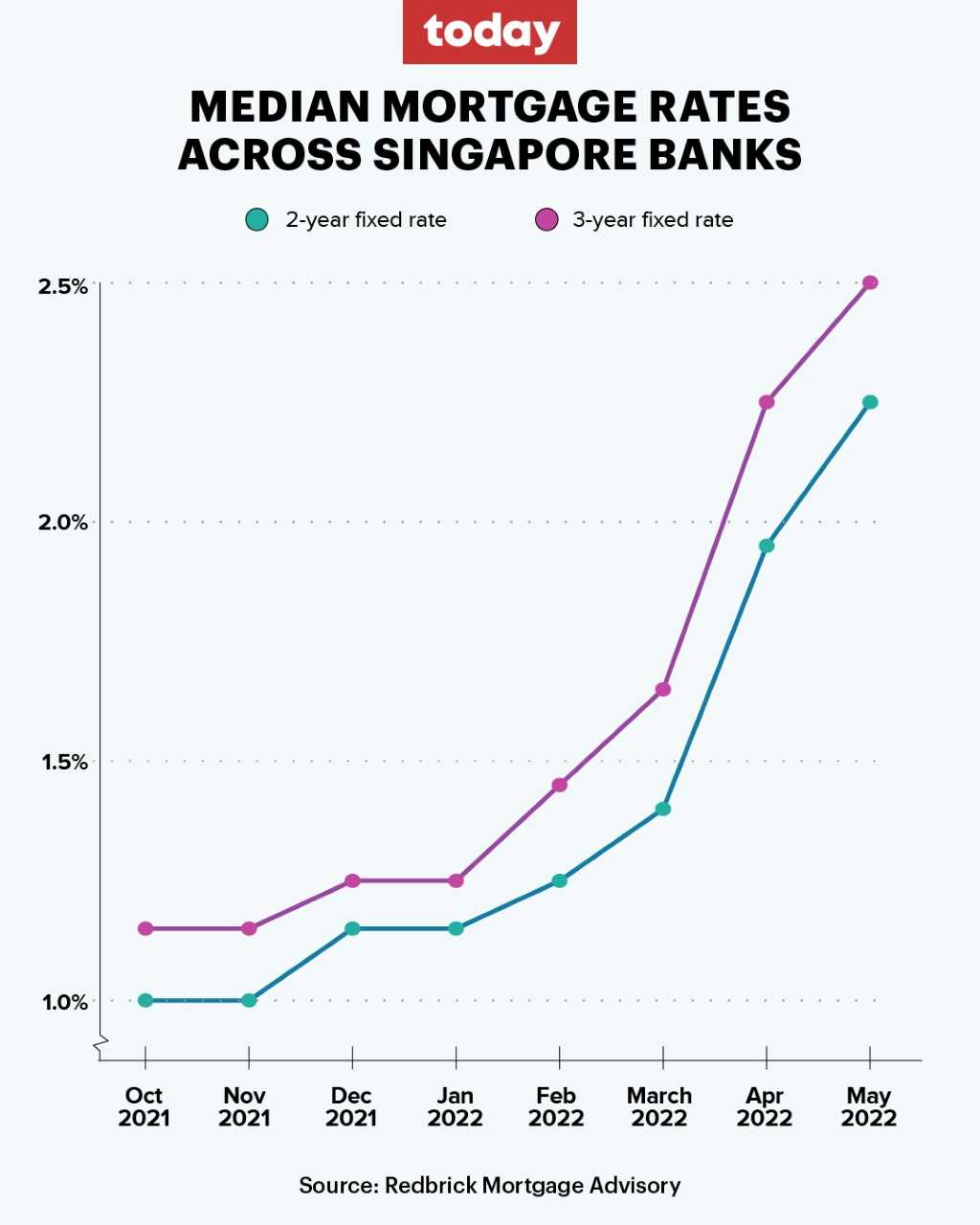

In general, two-year and three-year mortgage loans which carry a fixed rate have seen median rates go up from about 1.5 per cent at the start of the year to more than 2.6 per cent, according to a CNA article last month.

As of Friday, the fixed rates for two-year home loan packages at DBS bank and OCBC are 2.75 per cent and 2.98 per cent respectively.

STILL MANAGEABLE, FOR NOW

With median mortgage rates climbing, banks and property experts earlier warned homebuyers to set aside sufficient savings as a "buffer" and to seek new loan packages or arrangements if necessary.

Despite this, Huttons Asia's senior director for research Lee Sze Teck told TODAY that he does not believe the rising interest rates on mortgages will affect demand for housing in general.

Altitude Real Estate's key executive officer Nelson Lim added that “there is always a market” for genuine buyers who need a home to live in rather than invest in.

Rising interest rates, he said, will only temper a buyer’s expectations of the kind of home they can purchase and the amount of money they can borrow.

“By and large…even though there's an increase in the interest rates, it is still affordable at this point,” said Mr Lim. “So I do not see interest rates as being a very big deterrence for people buying property.”

Agreeing, Ms Christine Sun, senior vice president of research and analytics at OrangeTee and Tie, said the interest rate hike has not affected the public housing resale market substantially, as the loan quantum of most HDB flats is not high, and most homeowners are not over-leveraged.

As for the private residential property market, she said most existing homeowners should be able to service their home loans now.

THE 3 PER CENT THRESHOLD

However, the rising interest rates offered by banks for home mortgages are more likely to be keenly felt once they edge past the 3 per cent mark, said the analysts.

Pointing out that the total debt servicing ratio (TDSR) threshold for property loans uses a stringent 3.5 per cent interest rate computation, Ms Sun said there should be sufficient buffer for rates to move before monthly mortgage obligations exceed borrowers' gross monthly income.

This would mean that the cost of borrowing will matter more for home buyers, which could affect their decision on how much to spend on a home purchase, or whether to buy one in the first place.

The TDSR refers to the portion of a borrower's gross monthly income that goes towards repaying the monthly debt obligations, including the loan being applied for.

In a bid to cool the housing market, the TDSR was lowered from 60 per cent to 55 per cent last December. This means that a person's total monthly loan payments, including mortgage loans, cannot exceed 55 per cent of his or her total gross income.

Ms Sun said should such a situation occur, more first-time borrowers may switch to an HDB loan pegged to 2.6 per cent, or paying down their loans to reduce their monthly instalment, if they are in the public housing resale market.

Ms Wong Siew Ying, head of research and content at PropNex Realty also said that some buyers who were previously eyeing private residential properties "may decide to play it safe and opt to purchase a resale flat, which is generally more affordable compared to a private condominium.

Altitude Real Estate's Mr Lim added that said buyers will only likely start doing their “calculations” once the interest rates go beyond 5 per cent because it will affect their disposable income.

Still, he was optimistic that those who genuinely need a home will be able to afford one if the interest rates remain within the 5 per cent range.

But they may be more restrained when it comes to picking larger-sized properties, or those on higher floors, which cost more, he said.

STRONG MARKET

Moving forward, the analysts expect both housing prices and the market to remain strong.

They projected that the number of resale flats that will be transacted this year will be between the range of 25,000 and 28,000, with resale prices for the rest of the year rising between 7 and 10 per cent from 2021.

Said Ms Sun: “As HDB continues to launch more BTO flats in the second half of this year, the increased housing supply will continue to draw demand away from the resale market, which may help to regulate the pace of price growth and tame market exuberance.”

As for the private residential properties, the analysts estimated that the prices of new homes, excluding executive condominiums, may rise by 6 to 9 per cent this year as compared with 2021, while around 9,000 to 10,000 units may be transacted.

Ms Sun added that for the resale market, prices in the whole of 2022 may increase by between 6 and 8 per cent from the previous year, and about 11,000 to 13,000 resale homes could be sold.

“Amid global headwinds, Singapore's robust economic growth and consistently high employment rate may help cushion homeowners from the impact of the global economic uncertainties,” said Ms Sun.

“Moreover, investors flocking to traditional save havens to preserve their capital may still park their money here as our property investment market is considered one of the safest and most stable in the world.”

Related topics

interest rate Property housing loans mortgage HDB flat condominiumStay in the know. Anytime. Anywhere.

Subscribe to our newsletter for the top features, insights and must reads delivered straight to your inbox.

By clicking subscribe, I agree for my personal data to be used to send me TODAY newsletters, promotional offers and for research and analysis.