S'pore mortgage rates roughly double in 6 months; set to rise further, say property analysts

SINGAPORE — Median mortgage rates have roughly doubled here over the last six months as the global effort by central banks to combat inflation through higher interest rates takes a toll on local home-buyers.

- Mortgage rates here have increased markedly in recent months as central banks worldwide hike interest rates to combat inflation

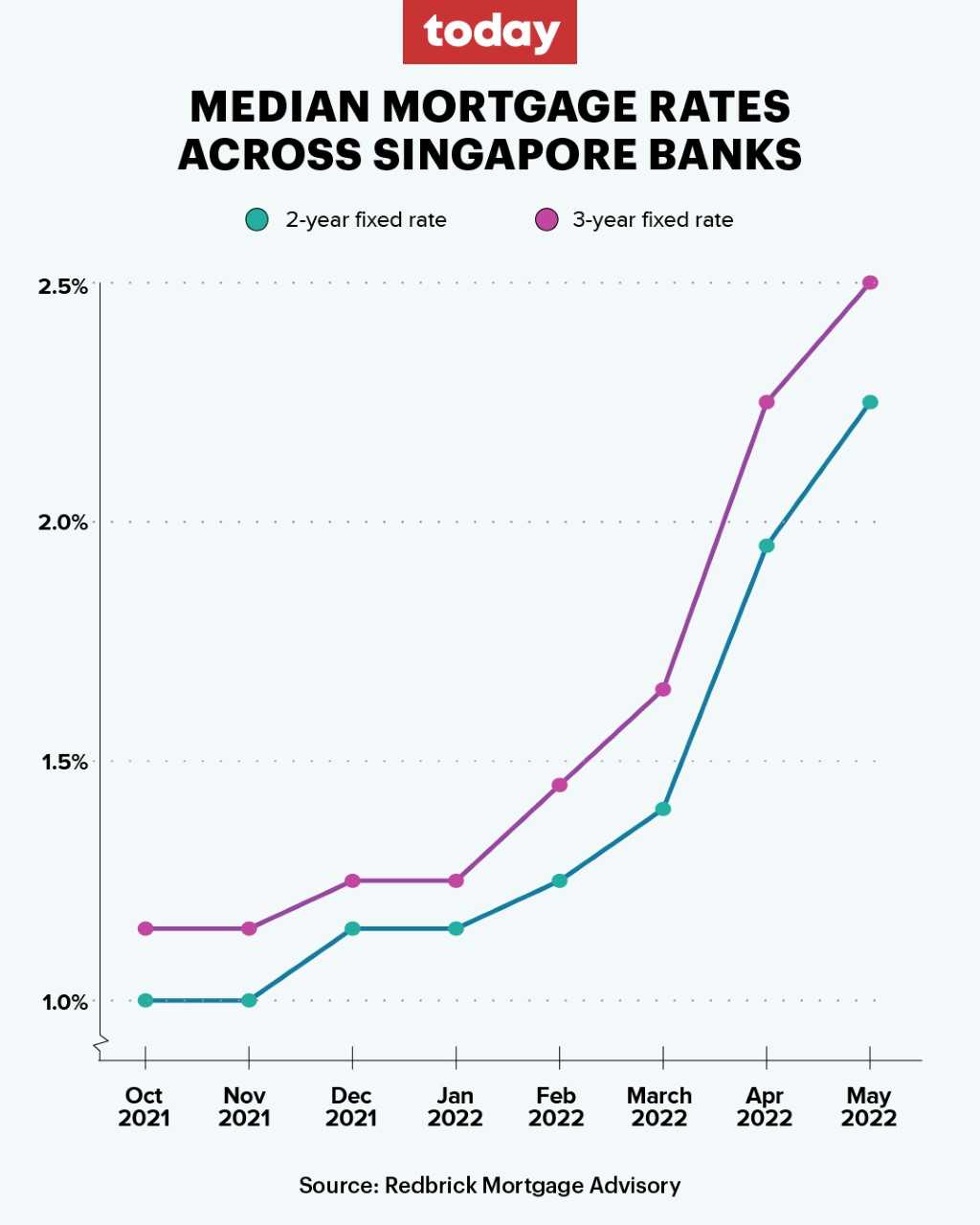

- For example, the median two-year fixed rate mortgage here rose 1.15 per cent in December last year to 2.25 per cent in May

- Analysts and banks warn borrowers to set aside sufficient savings as a "buffer" and to seek new loan packages or arrangements if necessary

- They expect mortgage rates to rise further in the months ahead

SINGAPORE — Median mortgage rates have roughly doubled here over the last six months as the global effort by central banks to combat inflation through higher interest rates takes a toll on local home-buyers.

Property analysts believe that further increases in mortgage rates are on the way, especially after the United States Federal Reserve announced its biggest rate hike since 2000 on Wednesday (May 4).

The relatively sudden spike in the cost of borrowing money has led analysts and banks to warn home-buyers to set aside sufficient savings as a "buffer" and to seek new loan packages or arrangements if necessary.

For a fixed two-year mortgage, the median rate across Singapore banks has increased from 1.15 per cent in December last year to 2.25 per cent in May, according to Redbrick Mortgage Advisory, a mortgage broker which compares interest rates from different banks.

For a three-year fixed mortgage, the rate in December was 1.15 per cent, while in May, this has more than doubled to 2.5 per cent.

Mortgages with floating interest rates pegged to benchmarks such as three-month Singapore Interbank Offered Rates (Sibor) and the Singapore Overnight Rate Average (Sora), have also risen, according to Redbrick.

The three-month Sibor has risen from 0.43 per cent to 1.05 per cent while the three-month Sora has increased from 0.15 per cent to 0.30 per cent compared to the previous quarter.

Sibor and Sora are benchmark rates that are used, for example, by banks here to set some mortgage rates for property buyers.

The hike in mortgage rates has been steeper in the past two months compared to the preceding four months. While the fixed two-year-mortgage rate rose to by 0.25 percentage points from 1.15 per cent in December 2021 to 1.4 per cent in March, it shot up by 0.85 percentage points to the current 2.25 per cent rate in May.

MORTGAGE RATES TO RISE ALONG WITH GLOBAL INTEREST RATES

Mr Nicholas Mak, head of research and consultancy at property agency ERA Realty, said that mortgage rates have been rising since six months ago as Singapore's interest rates fluctuate in tandem with global interest rates.

This is because Singapore's central bank, the Monetary Authority of Singapore, controls inflation by managing the country's exchange rate against its main trading partners, and does not directly set interest rates.

Interest rates in Singapore, and globally, were relatively low at the end of last year as they had largely remained that way through the pandemic, said Mr Mak.

“When Covid started two years ago, it was expected there would be economic slowdown, so to save the economies all over the world, central banks kept interest rates low. But interest rates (were expected) to go up ever since inflation started to rise.Mr Nicholas Mak, head of research and consultancy at property agency ERA Realty”

"When Covid started two years ago, it was expected that there would be economic slowdown, so to save the economies all over the world, central banks kept the interest rates low," said Mr Mak. "But there have been expectations for interest rates to go up ever since inflation started to rise."

But earlier this year, as economies around the world opened up and people started spending more money, central banks raised interest rates so as to slow demand and take pressure off prices.

As Singapore's economy, including its money market, is closely tied to global trends, this meant Singapore banks pushed up their interest rates, including mortgage rates.

The sharper rise in mortgage rates in the last two months was due in part to worsening inflation worldwide, partly driven by an energy crunch caused by Russia's invasion of Ukraine and the response of central banks to raise interest rates.

The US Fed's increase of half a percentage point on Wednesday was closely watched because the US is the world's largest economy and the US dollar is the world's "reserve currency".

"Some banks have been adjusting the interest rate upward after the Fed announcement," said Mr Steven Tan, chief executive officer of real estate agency OrangeTee & Tie. "Interest rates would likely continue to move up due to inflation's persistence."

For instance, Mr Tan forecasts that the two-year fixed mortgage rates will rise from the current 2.25 per cent to 2.75 per cent at its highest.

Ms Jo’An Tan, associate director of Redbrick Mortgage Advisory, expects the three-month Sora rates to rise from 0.3 per cent to about 1 per cent in the coming months, and for the three-month Sibor rate to jump from 1.05 per cent to 1.6 per cent.

WHAT SHOULD HOMEBUYERS TAKE NOTE OF?

Banks and property analysts told TODAY that homeowners first need to ensure that they have enough savings to tide through any change in mortgage rates.

One key reason is that some banks have been changing the terms of their packages. For instance, Mr Tan said that many foreign banks have recently stopped offering fixed rates.

"It is always advisable to go back to their own banker to assess their current package status," he said.

Mr Nelson Neo, head of home financing solutions at DBS Consumer Banking Group, said that borrowers should set aside sufficient funds as "a buffer in case of further interest rate hikes or any unforeseen circumstances".

Agreeing, Ms Maryanne Phua, head of home Loans at OCBC Bank, said that borrowers should regularly review their mortgage plans.

"For consumers with existing mortgages, it is beneficial to review their existing mortgage from time to time, taking a holistic approach in terms of pricing, service and terms of their loan," she said.

Upon reviewing their current loans, homeowners can consider refinancing their mortgages, which means paying off their existing loan and replacing it with a new one.

Responding to TODAY, a Maybank Singapore spokesman said that its customers can also approach the bank should they wish to reprice their loans after their lock-in period.

Mr Neo from DBS said that homeowners seeking to refinance their home loans are "encouraged to approach their existing banks to check the terms of their home loans, as well as if there will be any fees imposed, such as for an early redemption".

Ms Christine Sun, senior vice-president for research and analytics at property agency OrangeTee & Tie, said that although refinancing can come with a penalty fee, it may be worth it in the long term if the difference in interest rates is big enough.

"They have to calculate whether it is worth paying the penalty, versus the increase in the monthly mortgages that they are paying," she said.

Mr Mak from ERA Realty added that it could also be worth it to pay off part of the loan at the present, assuming that the homeowner has sufficient savings.

"That way, they won't have a huge outstanding loan," said Mr Mak. "Because the interest is charged from whatever outstanding loan that is."

For example, the savings account where a borrower parks his savings could be paying 0.5 per cent a month, while the mortgage loan interest rate could be increasing by a much larger percentage.

"If you're paying a higher mortgage (interest rate) and your savings account interest rate is so low, you can think of paying part of the loan."

Mr Paul Wee, vice president of FinTech at PropertyGuru Group, said that borrowers can also look into restructuring their loans, such as by extending their loan tenure or considering using more Central Provident Fund (CPF) funds in their home loan servicing.

"They may also take into account future plans, such as planned retirement, family plans, for example, and build in these requirements into their (mortgage) plans," he added.

FOR PROSPECTIVE BUYERS: FLOATING OR FIXED MORTGAGES?

For prospective home buyers, whether to choose a fixed rate or floating mortgage depends on their risk appetite, as both packages have their pros and cons.

Mr Mak said that traditionally, fixed rate mortgage rates, while more stable for the borrower, are usually set at a higher rate than that of a floating mortgage.

"It really depends on what's the risk appetite of the borrower, it the borrower says they'll take the bet and stick with floating rate with the belief that it will not go up that much... there is no right answer."

Ms Tan from Redbrick said that borrowers need to look at the long term and not at the rates in front of them. This is because floating rates can rise to exceed two-year fixed rates in that two-year period.

"At this point, one could still choose between a floating interest rates at 0.95 per cent or a fixed interest at 2.25 per cent," she said. "The question one would need to ask before deciding is how high will interest rates rise to."

Banks are also offering the choice for customers to have both fixed and float rates in their packages to "average up the risk", said Mr Tan from OrangeTee & Tie.

For instance, DBS Bank has a package where borrowers may park a portion of their loan amount under a fixed rate package while the remainder will be under a floating rate package.

Related topics

mortgage Property interest rate banksStay in the know. Anytime. Anywhere.

Subscribe to our newsletter for the top features, insights and must reads delivered straight to your inbox.

By clicking subscribe, I agree for my personal data to be used to send me TODAY newsletters, promotional offers and for research and analysis.